Download the notebook here!

Interactive online version: ![]()

Uncertainty propagation¶

We show how to conduct uncertainty propagation for the EOQ model. We can simply import the core function from temfpy.

[1]:

import matplotlib.pyplot as plt

import matplotlib as mpl

import seaborn as sns

import chaospy as cp

from temfpy.uncertainty_quantification import eoq_model

from econsa.correlation import gc_correlation

Setup¶

We specify a uniform distribution centered around \(\mathbf{x^0}=(M, C, S) = (1230, 0.0135, 2.15)\) and spread the support 10% above and below the center.

[2]:

marginals = list()

for center in [1230, 0.0135, 2.15]:

lower, upper = 0.9 * center, 1.1 * center

marginals.append(cp.Uniform(lower, upper))

Independent parameters¶

We now construct a joint distribution for the the independent input parameters and draw a sample of \(1,000\) random samples.

[3]:

distribution = cp.J(*marginals)

sample = distribution.sample(10000, rule="random")

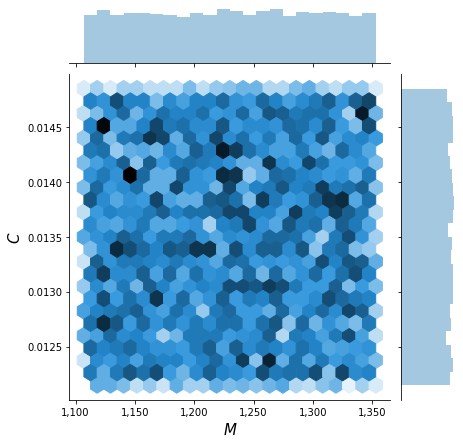

The briefly inspect the joint distribution of \(M\) and \(C\).

[5]:

plot_joint(sample)

We are now ready to compute the optimal economic order quantity for each draw.

[6]:

y = eoq_model(sample)

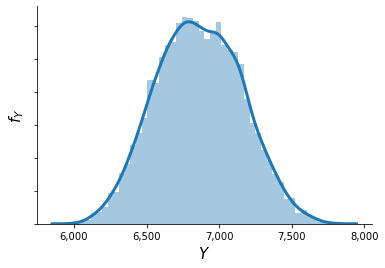

This results in the following distribution \(f_{Y}\).

[8]:

plot_quantity(y)

Depdendent paramters¶

We now consider dependent parameters with the following correlation matrix.

[9]:

corr = [[1.0, 0.6, 0.2], [0.6, 1.0, 0.0], [0.2, 0.0, 1.0]]

We approximate their joint distribution using a Gaussian copula. This requires us to map the correlation matrix of the parameters to the correlation matrix of the copula.

[10]:

corr_copula = gc_correlation(marginals, corr)

copula = cp.Nataf(distribution, corr)

We are ready to sample from the distribution.

[11]:

sample = copula.sample(10000, rule="random")

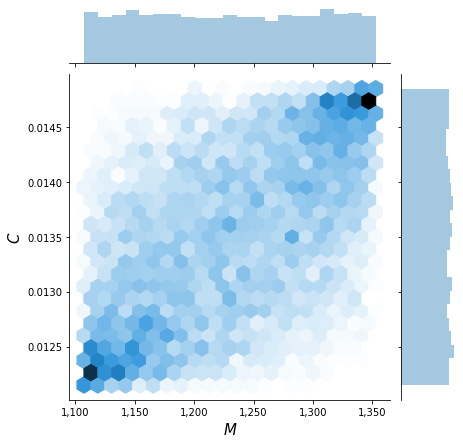

Again, we briefly inspect the joint distribution which now clearly shows a dependence pattern.

[12]:

plot_joint(sample)

[13]:

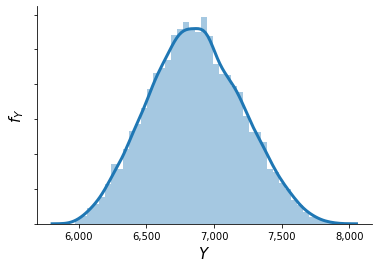

y = eoq_model(sample)

This now results in a distribution of \(f_{Y}\) where the peak is flattened out.

[14]:

plot_quantity(y)