Uncertainty propagation¶

We start from a probabilistic model for the input parameters that is informed by, for example, expert knowledge or the outcome of a calibration. We treat the model parameters \(\mathbf{X}\) as a simple random vector with a joint probability density function \(f_{\mathbf{X}}\). We are not particularly interested in the uncertainty of each individual parameter of the model. Instead we seek to learn about the induced distribution of the model output \(Y\) as the uncertainty about the model parameters \(\mathbf{X}\) propagates through the computational model \(\mathbf{M}\). We want to study the statistical properties of \(Y\).

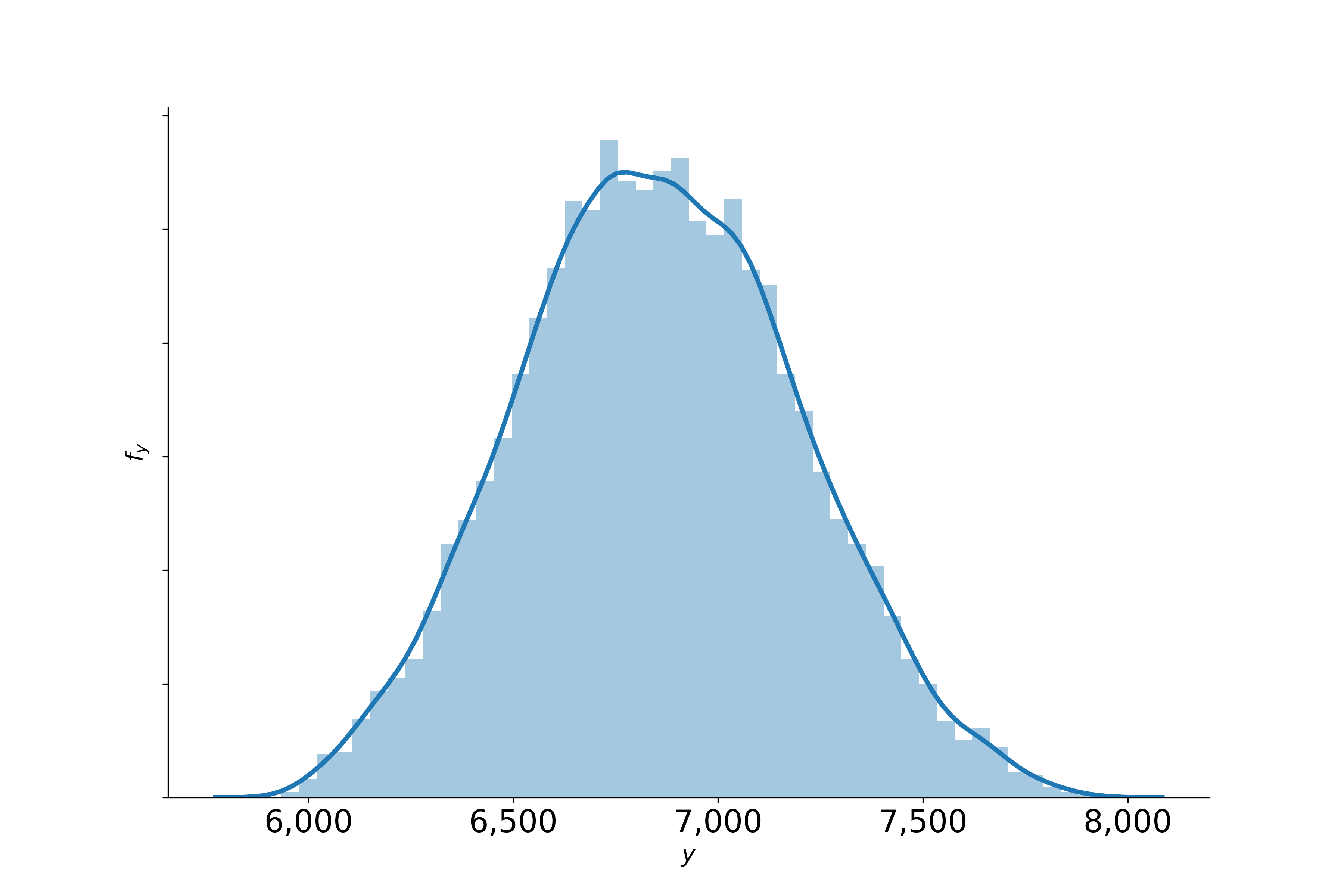

We now return to the example of the EOQ model. We specify a uniform distribution centered around \(\mathbf{x^0}=(M, C, S) = (1230, 0.0135, 2.15)\) and spread the support 10% above and below the center. We solve for the optimal economic order quantity \(Y\) for \(1,000\) random input parameters and end up with the distribution \(f_{Y}\) below.